Common Myths: Demystifying Credit Card Credit Score Factors

In today’s financial landscape, understanding your credit score is crucial. It’s a three-digit number that represents your creditworthiness to lenders. It provides insight into your credit history, repayment habits, and overall financial responsibility. Your credit score is a key factor in determining whether you qualify for loans, credit cards, and favorable interest rates.

Credit Score Factors, Myths & Impact of Credit Cards

Understanding Credit Score Factors

What is a credit score?

Your credit score can determine everything from the interest rates you’re offered, credit card approvals, auto loans, or whether or not you qualify for that new apartment. It’s a numerical representation of your creditworthiness. It is calculated based on information from your credit report, including your payment history, credit utilization ratio, length of credit history, new credit inquiries, and credit mix. Credit scores typically range from 300 to 850, ranging from poor to excellent credit.

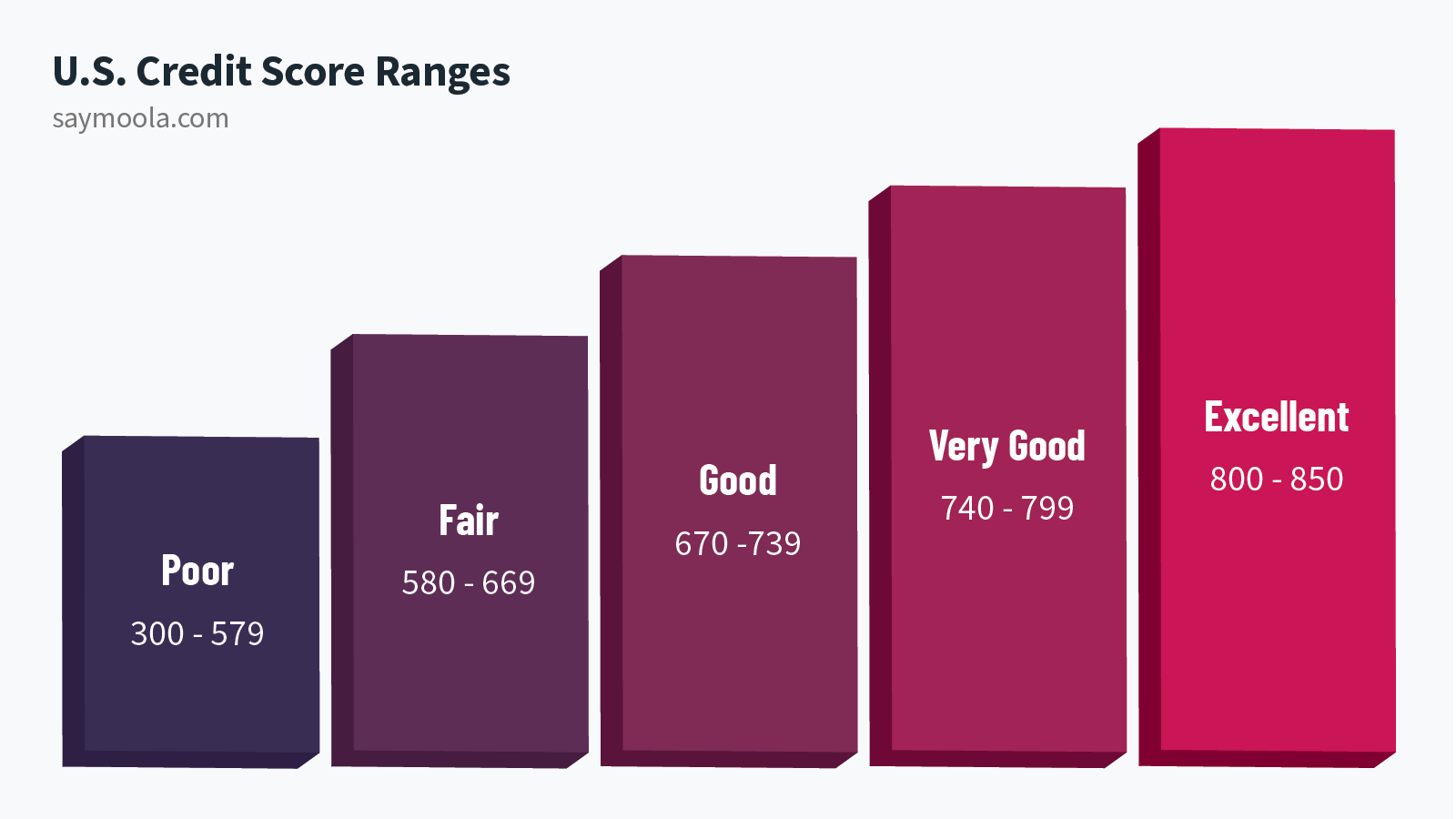

The range of credit scores in the U.S.:

- 300 to 579: Poor

- 580 to 669: Fair

- 670 to 739: Good

- 740 to 799: Very good

- 800 to 850: Excellent

The 3 credit bureaus

There are three major credit reporting agencies: Experian, TransUnion, and Equifax. These are the big three of your credit report, keeping tabs on everything from your payment history to your outstanding debts. When it comes to your credit score, most lenders use a scoring model known as VantageScore or FICO score, which takes into account the information from these agencies. You can create an account with each of these agencies to see your current score at any time.

How to build good credit

Building credit can seem like a daunting task, but it’s actually pretty simple if you know what you’re doing. In a short time, you can start to see improvements in your credit score. One key factor in building good credit is the average age of credit, so try to keep your oldest accounts open. Some parents will even open accounts for their children at a young age so the timeline of building credit starts sooner. Other important factors include low credit card debt and paying your bills on time to avoid presenting yourself as a risk and damaging your credit. By maintaining healthy personal financial management and making responsible decisions, you can work towards a higher score.

What affects your credit score

Several key factors influence your credit score. These include things like payment history, credit usage, length of credit history, types of credit accounts, and new credit inquiries (referred to as hard inquiries). Maintaining a history of on-time payments, using credit responsibly, and keeping credit card balances low can all positively impact your score.

The primary credit factors and how they weigh on your score:

- Payment history: 35% of score

- Amount of debt: 30% of score

- Length of credit history: 15% of score

- Amount of new credit: 10% of score

- Credit mix: 10% of score

What doesn’t affect your credit score

Contrary to popular belief, factors like your age, income, race, and marital status do not directly impact your credit score. Your score is based solely on your credit history and financial behavior. Similarly, checking your score or obtaining a copy of your credit report does not hurt your credit score; these are considered soft inquiries.

Debunking Credit Card Myths

Myth #1: Carrying a balance

Many people believe that maintaining a balance on their credit card can enhance their credit score. However, the reality is that the most effective way to demonstrate responsible credit behavior is by fully paying off your statement balance each month. It’s much better to avoid carrying a balance that is subject to interest charges. Buy what you need and can afford.

Myth #2: Applying for new credit

Another misconception people have is that applying for a credit card will negatively impact their credit score or prevent them from getting approved for a premium card. However, the truth is that although a new credit line may cause a slight decrease in your score temporarily, it will not have a significant impact in the long run. What can actually harm your score is the number of recent credit checks, as it is advisable to have no more than 5 inquiries within the past year.

Myth #3: Number of credit cards

The majority of credit card issuers have restrictions on the number of new credit cards you can apply for within a specific timeframe. However, holding multiple cards will not harm your credit rating as long as you demonstrate responsible usage. Having more than a few cards can increase your total credit limit and lower your credit utilization ratio. It can prove your ability to manage a large amount of credit effectively, which in turn can improve your credit score.

Myth #4: Closing unused credit cards

You may think that it’s a good idea to close credit cards that you’re no longer using. However, because the length of credit history is so important to your overall credit score, the best approach is to keep cards open – especially your oldest cards. These will weigh heavily on your average age of credit, which you want to be as old as possible. Consider no annual fee cards that can stay open, as you may eventually want to cancel cards with a fee.

Myth #5: Checking your credit score

If you are checking your credit for personal reasons with one of the three credit bureaus, it won’t harm your credit. It’s considered a soft inquiry as long you’re not applying for a credit line or loan, as those are hard inquiries that do appear on your credit report. Simply monitoring your credit score regularly can help you stay on top of your financial health, and alert you to any shady activity.

Deeper Dive: Impact of Credit Card Usage

What is a credit utilization ratio?

When it comes to credit card usage, one crucial factor to consider is your credit utilization ratio. This ratio is the amount of total credit you are currently using compared to your total credit limit on all your cards. For example, if you have a $50,000 credit limit, and your most recent monthly balance is $5,000, then your utilization ratio is 10%. Maintaining low credit usage is essential for a healthy credit score.

Lenders often prefer to see a ratio of less than 30%, as it indicates responsible credit management and lower financial risk. Better yet, if you are using less than 10% or even 5% of your available credit, it will bode even better for your credit score. On the other hand, if you are using 0% of your available credit, new credit applications may be denied due to lack of usage, especially with a card issuer where you already have a card account established.

How does using a credit card impact my score?

Using a credit card can have a direct impact on your credit score. It affects factors such as credit utilization ratio, payment history, and credit history, all of which are important in scoring models like FICO and Vantagescore used by lenders.

Will having a high credit limit on my credit card hurt my score?

Having a high credit limit on your credit card can actually be beneficial for your credit score if you maintain a low credit utilization ratio. It can show good credit management and increase your available credit.

Can applying for multiple credit cards at once affect my score?

Applying for multiple credit cards in a short period may result in multiple inquiries on your credit report, which can have a negative impact on your credit score. It’s important to space out your credit inquiries and follow any rules each bank considers for approvals.

How many credit cards is too many?

Many consumers only have 1-2 credit cards. And on the other end of the spectrum, some people have dozens of cards. So what’s the limit? The answer is different for everyone. At the end of the day, if you’re taking the factors we’ve discussed into account, over time you could amass as many cards as you are comfortable managing.

Do all credit card issuers report to credit bureaus?

Most credit card issuers report your personal credit card account activity to credit bureaus. The exception is business credit cards which are usually not reported to the bureaus. Information from your revolving credit accounts (with or without a balance owed) is used to calculate your credit score, which is then viewable to any new lender inquiries.

Credit Card Credit Score Wrap-up

In conclusion, understanding the factors that influence credit scores is essential for improving financial well-being. By managing credit responsibly and maintaining a good credit score, you can access better financial opportunities. It’s important to debunk these common credit score myths and focus on the FICO score distribution key factors that contribute to a favorable rating.

Remember, credit card issuers are happy to extend credit to you based on how you fit their requirements, as they stand to profit from transactions and fees. It is your responsibility to use this spending power wisely. Only buy what you would normally need and have the means to pay back, and always pay off your statement balance to avoid interest charges. If you play your cards right, there is a bounty of rewards and benefits you stand to gain from credit cards.

Share this article:

Pingback: Simple Cash Back: Best Catch All Credit Cards for a 2x Flat Rate (or More)