Capital One Venture X Approval: Why Your 800 Credit Score Isn’t Enough

I’ve seen plenty of 780+ credit scores denied for the Capital One Venture X, while someone with a 720 score is approved. If you think Capital One’s underwriting is just about credit scores, you’re about to get a reality check (possibly in the form of a denial letter).

The Venture X has become notoriously difficult to get approved for in the points and miles community. Capital One’s algorithm is looking for something very specific, and spoiler alert: it’s not just whether you pay your bills on time.

Let me break down what actually matters when Capital One reviews your Venture X application, because understanding these factors is the difference between adding a premium rewards card to your wallet and wondering why your excellent credit wasn’t good enough.

The approval factors and data points in this guide are drawn from extensive analysis of real-world applicant experiences across Reddit communities (r/CreditCards, r/Venturex), myFICO Forums, and credit card resources such as Doctor of Credit and The Points Guy. While individual experiences vary, these patterns emerge consistently across hundreds of reported applications.

In This Guide

The Single Biggest Factor for Capital One Venture X Approval

Here’s the truth: recent new credit card activity is responsible for over 70% of Capital One Venture X denials. Not income. Not credit score. Your card opening velocity.

Capital One is extremely sensitive to new accounts. If you’ve been hitting SUBs hard over the past two years, you’re probably going to have a bad time:

6+ cards in 24 months:

Your approval odds just fell off a cliff

3-4 cards in 24 months:

You’re in the danger zone where many denials happen

2 or fewer cards in 24 months:

Now we’re talking

The timing of your most recent opening matters too. Applicants report significantly greater success when their last card was opened 6-8 months ago than when it was opened 2-3 months ago. Capital One wants to see that you’re not just churning through bonuses.

I know this stings if you’re deep in the points game, but Capital One’s algorithm is specifically designed to avoid “bonus chasers.” They want customers who’ll actually use the Capital One Venture X card long-term, not someone who’ll hit the MSR and sock-drawer it.

Capital One Credit Card Application Rules You Need to Know

Beyond your overall velocity, Capital One has some specific timing rules:

The 30-day limit:

Don’t even think about applying for two Capital One cards within 30 days. This is a strict policy and will result in wasted hard inquiries on your report.

The 6-month rule:

Capital One generally limits approvals to one card per six-month period. Recent data points suggest this might have softened to around 90 days, but I wouldn’t bet my application on it.

The 48-month bonus rule:

Capital One won’t approve you for another Venture X SUB if you’ve earned one within the last four years. (This applies to the current 75,000-mile offer.)

Credit Profile Factors That Impact Venture X Approval

Hard Inquiries and Why Capital One Cares

Unlike some issuers that barely glance at inquiries, Capital One pays attention. And here’s the kicker: they pull all three credit bureaus (Experian, Equifax, TransUnion), meaning you’ll see three hard pulls from one application.

6+ inquiries in 24 months:

Expect to see “too many recent inquiries” in your denial letter

2-4 inquiries in 24 months:

Generally acceptable range

This is one reason I’m more selective about Capital One applications than Chase or Amex.

The Total Accounts Factor Nobody Talks About

Here’s where Capital One gets really different from other issuers. They actually care about your total number of open revolving accounts, not just recent ones.

19+ open accounts:

Approval odds drop to basically zero

10-18 open accounts:

Moderate to high denial risk

Under 10 accounts:

Significantly better odds

I’ve personally kept my total account number in mind when deciding whether to close older cards I’m not using. If you’re sitting at 15+ open cards and eyeing the Venture X, you might want to do some pruning first (just be mindful of how closures affect your credit utilization and average age of accounts).

Capital One appears to target customers with “cleaner” credit profiles who will generate sustained spending, not power users with 20 open cards.

Credit History Length and the $10,000 Credit Limit Requirement

The Venture X requires a minimum $10,000 credit limit (per Visa Infinite requirements), which means Capital One needs confidence in your credit profile.

Under 1.5 years of credit history:

Very low approval odds

2-3+ years:

Significantly better odds

If you’re new to credit, building up your credit history before applying for the Venture X is essential. This isn’t a starter premium card.

Income, Debt, and Credit Utilization Requirements

Capital One doesn’t publish income minimums, but here’s what matters:

Data points show approvals ranging from $37,000 to $250,000+ annual income, so it’s not about hitting some magic number.

What kills applications is high debt-to-income ratios. Big mortgage, student loans, auto loans—even with high income, these can trigger denials.

Credit utilization is another factor. Multiple denial letters cite “too many accounts with balances.” Keep utilization under 10% for 1-2 months before applying.

Improving Your Capital One Venture X Approval Odds

The Pre-Approval Tool: Worth Checking, But Don’t Count On It

Capital One has a Venture X-specific pre-approval tool, and when it shows pre-approval, your odds are supposedly around 90%.

Here’s the thing: I’ve never personally seen a Venture X pre-approval show up, even when checking that specific URL. Instead, I see Savor, Quicksilver, or VentureOne cards (which, given my card opening history, probably means I wouldn’t be approved for Venture X anyway).

Check the tool, but if you don’t see the Venture X, don’t be discouraged—just make sure the other factors I’ve covered align with your profile before applying.

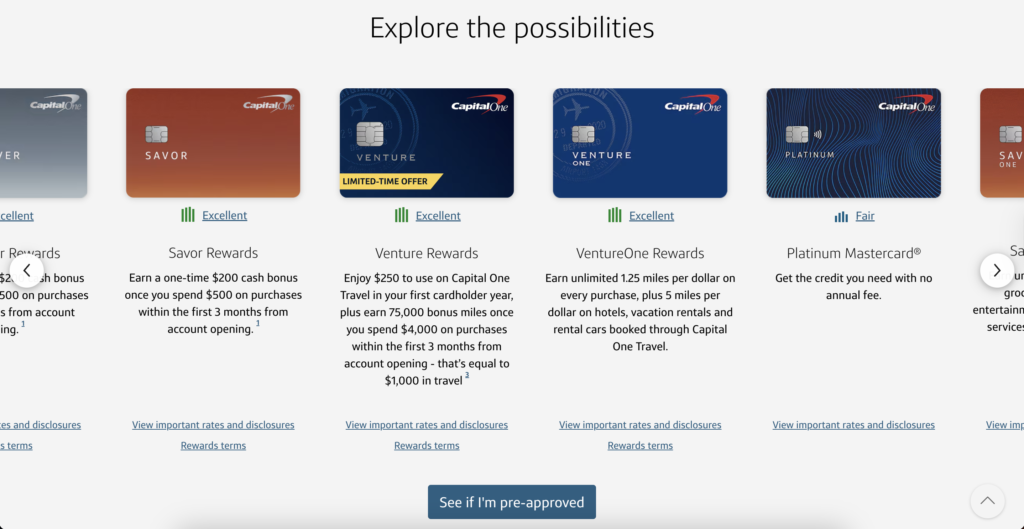

The Existing Capital One Relationship Factor

Having an existing Capital One card may improve your approval odds, though it’s not required. The relationship provides Capital One with data about your spending patterns and payment behavior.

One important note: Capital One has an unofficial “two personal card limit” for their core products (Venture, Savor, Quicksilver families). If you already have two Capital One personal cards, you might need to close one before applying for the Venture X. Co-branded and secured cards don’t count toward this limit.

What About Getting a Capital One Checking Account First?

Doesn’t help. Neither does having an 820 credit score or a $200K income if you’ve opened six cards in the past year.

Capital One’s algorithm prioritizes profitability over pure creditworthiness. They’d rather approve someone with a 740 score and two total credit cards than an 800-score churner with 20 open accounts.

How to Get Approved for the Venture X: Smart Application Strategy

If you want the Venture X, here’s my recommendation:

- Cool your velocity: Wait at least six months after your last card opening. Ideally longer.

- Check your total number of accounts: If you have over 15 open cards, consider closing some you don’t use.

- Get your utilization down: Under 10% across all cards; let it report for 1-2 statement cycles.

- Unfreeze all three bureaus: Capital One needs access to all three reports and will deny if any are frozen.

- Consider the upgrade path: If you have an existing Capital One Venture card (the non-X version) for 12+ months, check for upgrade offers. You’ll skip the hard pulls, though you’ll also forfeit the sign-up bonus.

Or just be patient. I know that’s not what points enthusiasts want to hear, but sometimes the best strategy is letting your credit profile calm down before going after that Venture X approval.

The Capital One Venture X rewards are compelling—$300 Capital One travel credit, 10,000-mile anniversary bonus, Priority Pass lounge access, Travel insurance, TSA PreCheck/Global Entry credit—and worth playing the long game to get approved rather than rushing in and getting denied. Whether you’re chasing the reward structure or the premium perks, patience with your application timing will pay off.

Learn about the general credit card application rules from all the major US card issuers.

Editor’s note: Opinions shared in this article are solely the author’s and do not represent the views of any bank, credit card issuer, hotel, airline, or other organization. The content has not been evaluated, approved, or endorsed by any of the mentioned entities. These are our recommendations but it isn’t financial advice. We may receive a commission if you click through any of the links in this article.

Share this article:

Pingback: Navigating Credit Card Application Rules: Chase 5/24, Amex Lifetime & More